Sublime

An inspiration engine for ideas

AI Phutures

Jesse Burkunk • 6 cards

My mini lectures in Quant Finance:

1- Deriving Black-Scholes via Itô's lemma (the dynaming hedging approach)

2- Why we don't use Black Scholes (my work with @EGHaug)

https://t.co/ff2AURSf3Z

Nassim Nicholas Talebx.comInvesting

Rob Berger • 4 cards

Ok I think I understand what my issue here is:

Imagine an at-the-money binary option with one day left to expiry. It will either payout $500bn or 0$ tomorrow. Such an option will have *infinite* delta. Stripe is that option https://t.co/NbTDVEkOf9

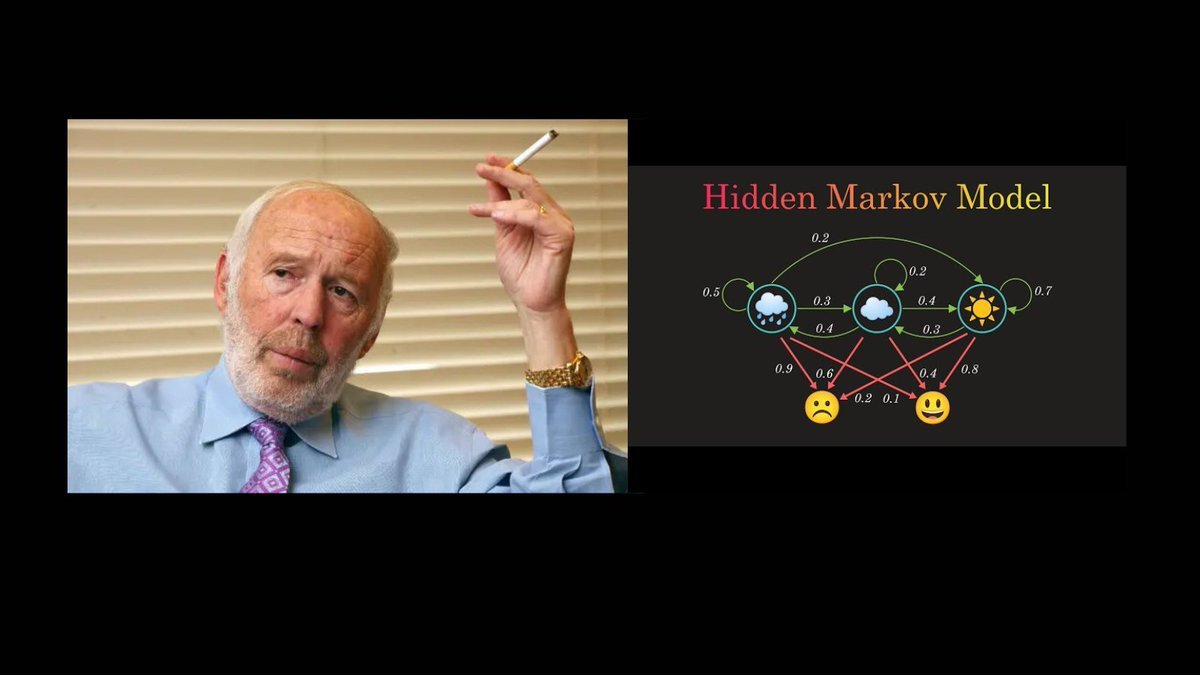

RenTec uses Hidden Markov Models in trading.

The technique generated 60% returns per year over 30 years.

One of the co-founders of RenTec's name is in the algorithm!

Here's how it works: https://t.co/aogI0bDtu7