Sublime

An inspiration engine for ideas

Donald Trump and Sanae Takaichi promise ‘golden age’ for US-Japan alliance

ft.com

From the @wsj article, “A $10 Billion Real-Estate Fund Is Bleeding Cash and Running Out of Options.”

The liquidity challenge facing this fund is attracting attention well beyond the investors in the fund and in the sector as a whole.

Its remedial actions — namely, the mix between more... See more

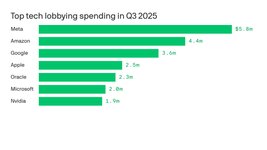

Just a moment...

axios.com

@GZuckerman is an excellent journalist and does real homework. #OldSchool

How FTX’s Sam Bankman-Fried Went From Crypto Golden Boy to Villain - WSJ https://t.co/NHCTh1YFRl

Mark W. Yusko - Two Point One Quadrillionx.comMarket Trends

Jin Kim • 2 cards

Journalism

Faith Hahn • 5 cards

“Every part of our financial and legal system at this point is devoted, singularly devoted, to keeping the status quo in place,” Harvard Law School professor Susan Crawford said in the webinar. “It will be difficult for us to adapt.”

Mark Gongloff • A $1 Trillion Time Bomb Is Ticking in the Housing Market - Bloomberg

Wealthfront has stalled out around $21 billion in assets under management (AUM) as it faces stiff competition from well-funded incumbents, and it still loses a lot of money. It charges only 0.25% of every dollar it manages for accounts with over $5,000.